Welcome the people you can't afford to lose.

WIMBY — Welcome In My Back Yard — helps you keep the people you can't afford to lose. You fund a forgivable down-payment loan so a senior employee can buy a house in your town, and it forgives a little more every year they stay. The tax math is handled so it's the smallest it can lawfully be, and the program is built on a clear rule that treats everyone the same — objective, documented, and defensible.

For the owner who knows everyone's first name.

If losing one person would genuinely hurt your business — and them leaving might mean their family moves out of town — this was built for you.

Specialty Trades

Roofing, parking-lot striping, HVAC, electrical — owner-operators whose business runs on a handful of irreplaceable crew leads. Give them a reason to stay.

Pediatric Clinics

Independent peds practices going head-to-head with hospital groups for skilled nurses and therapists. Give your best people a reason to put down roots in your town.

Occupational Therapy Clinics

OT practices where one therapist leaving can strand a caseload. Turn tenure into a house in town your team can bank on.

Physical & Speech Therapy Clinics

Independent PT and SLP practices where a senior clinician leaving means families on a waitlist and the hospital system picking up the referrals. Give your best therapists a reason to build their life around your clinic.

What a defensible program looks like.

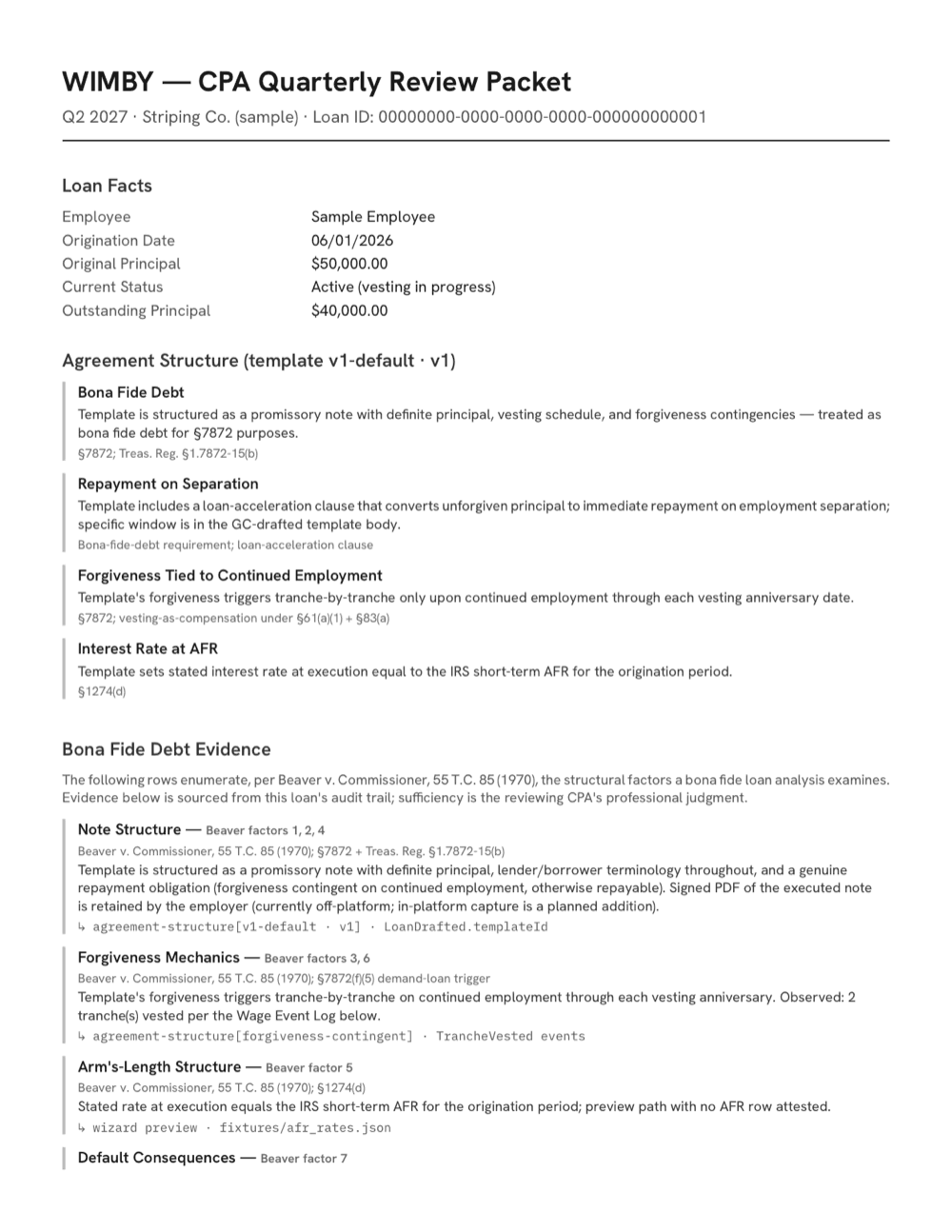

One objective rule, applied to everyone, with the paperwork to show it — that is what makes a housing-assistance program defensible. The packet below is the documented record WIMBY produces for every loan; your CPA reviews and signs it, not a summary she has to take on faith.

- AFR sourced from the IRS Rev Rul for the origination month — no surprise rate at year-end.

- W-2 wage events ready for Gusto payroll — direct push is a planned addition.

- Attorney-drafted loan documents for CA, TX, NY, FL, and IL.

- Quarterly CPA packet — reviewed before April, not during it.

One objective rule, applied to everyone and documented, makes a program more defensible than help handed out case by case — though it isn't a guarantee, and a neutral rule that ends up shutting out a protected group can still be a problem, so check yours with your own advisors. WIMBY structures the program and your CPA reviews and signs off; we don't provide tax advice.

What would it cost to replace them?

Losing a senior person costs far more than their salary — recruiting, lost ramp-up, and the work that waits while you rehire. Size the stake for your own team.

$30k – $250k

~$48,750 to replace a $65k crew lead

Industry estimates span 50–200% of salary — about $32,500–$130,000 for this role.

How we calculated this

An estimate: the salary you entered × a conservative, industry-specific replacement factor, shown as a range because published figures vary. Sources:

WIMBY structures it as a documented, objective program — a different legal position than an ad-hoc handshake loan.

Join the founding cohortWhat this changes for you as the owner

Five specific things you get that a holiday bonus or a 401(k) match doesn't deliver.

“The team was confused why it was on their W-2.”

Cash bonuses and most gift cards are always W-2 taxable — and your employee finds out at year-end. The forgivable-loan structure puts the right withholding on each tranche as it vests, so there's no surprise in January.

DIY 0% loans expose you to phantom interest. Yours is set at the IRS minimum.

§7872 deems a below-AFR employer loan to be paying foregone interest as W-2 wages every year, whether cash moved or not. WIMBY applies the IRS's minimum allowed rate — the AFR — at origination so the phantom interest is the smallest it can lawfully be. Your CPA reviews the per-period rate before each year's payroll.

You get a documented program, not a paper trail of a guess.

Promissory note, AFR snapshots, vesting schedule, W-2 wage events ready for payroll, quarterly summary line-itemed for QuickBooks reconciliation — one objective rule applied the same way every time, with the record to show it. Your accountant reviews and signs off — no two-week wait, no rebuilding the math from scratch.

Forgiven principal is a deductible business expense, not a gift out of your pocket.

Each year a tranche vests, that amount flows through payroll as W-2 wages — which means you take a §162 wage deduction on every dollar you forgive. Same net cost as a cash bonus; spread over five years instead of one.

Something you can quote to the candidate, not just to the person already on payroll.

A hospital system can outbid you on starting salary. They can't offer a five-year vesting loan that ties your senior clinician to your clinic. You can — and you can say so on the first call.

What WIMBY isn't

- Not a benefits platform — we do one thing.

- Not investment or tax advice — your CPA reviews; we make her job easier.

- Not a substitute for your attorney — loan documents are attorney-drafted; your counsel signs off.

- Not a way to dress up a cash bonus — cash and most gift cards are always W-2 taxable, and we don't change that.

- Not a loan to you — you fund the principal from cash; we structure, document, and account for it.

How it works

The quiet, one-at-a-time favor is the hardest kind to explain later — to the tax side, or to the next person who asks “why them and not me?” A documented program runs one rule for everyone — the answer’s in the file, not your memory.

Tell us who you want to keep

Share which employees you want to help buy a house — we don't need SSNs or personal financial data. Just tenure, role, and the retention window you're aiming for.

We structure the loan

WIMBY generates the forgivable down-payment loan structure from your inputs, produces the W-2 wage events for your payroll system and the line items for your QuickBooks reconciliation, and provides the documents your attorney reviews. We're the software; your counsel signs off on the legal terms.

Your best people stay

Your employee gets a meaningful down-payment loan that forgives with tenure. You track it all in one dashboard — no spreadsheets, no manual journal entries, no surprise W-2 in January.

Keep the people you can't afford to lose.

Join the founding cohort — we open the pilot to the first 10 owners soon, and you'll hear from us the moment it's your turn.

The first 10 owners get a personal welcome call from me before the pilot opens. Everyone on the waitlist hears from me directly — not a drip sequence. — Damon, WIMBY